Optex Systems: When the Primes Win, This One Follows

A $40M defense subcontractor compounding quietly under the radar — backed by backlog, ROIC, and multi-year contracts

Estimated Reading Time: 8 Minutes

Tariffs are back.

The S&P’s correcting — but valuations haven’t. Recession warnings are everywhere.

If you’re new to this, the message seems to be: buy the dip, trust the multiple, and if there’s a chart with arrows, even better.

I’m not convinced. The median stock still trades like it’s 2021.

And the index might need to fall another 30% before it even starts to look historically cheap.

But here’s the thing: you don’t have to own the index.

You can own this instead:

$40M market cap defense subcontractor with no debt

Trades at ~8x 2025E NOPAT

Revenue CAGR: 24%, NOPAT CAGR: 45% (3-year average)

15–20% ROIC, with a decade-long reinvestment runway tied to multi-year defense programs

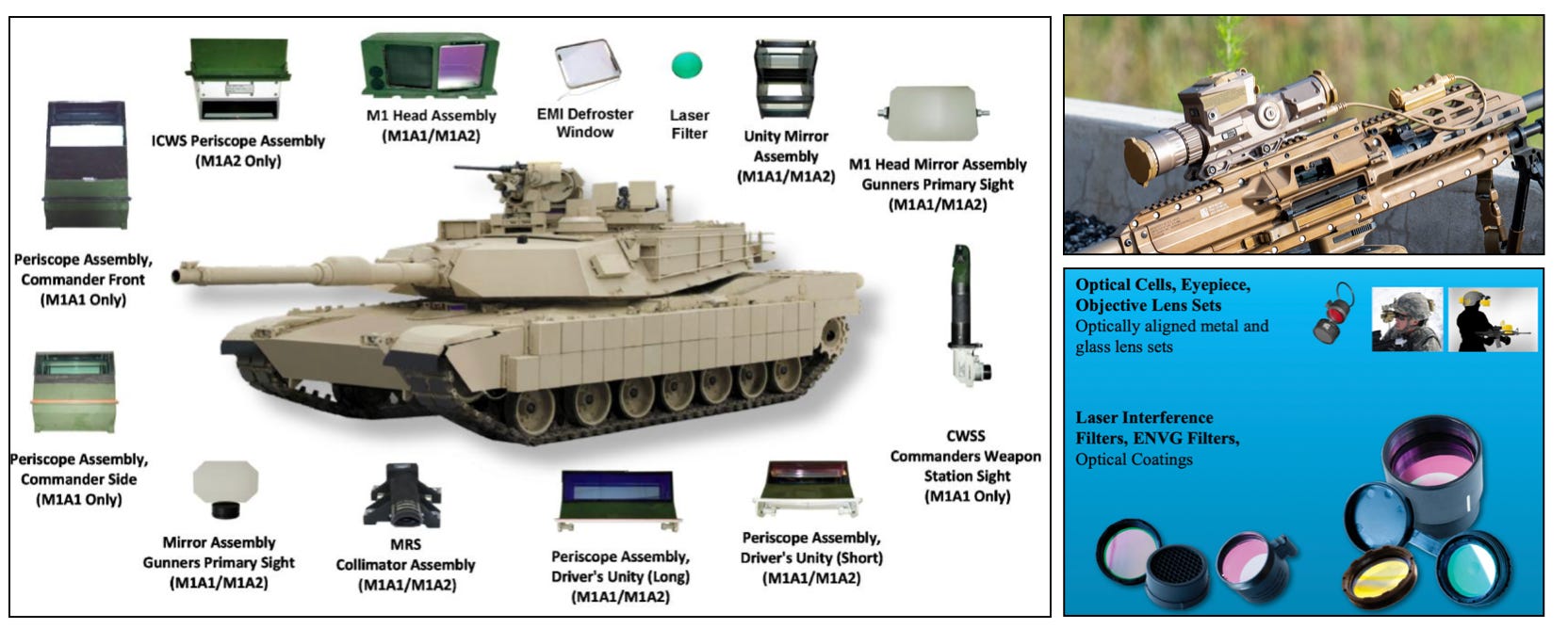

Direct exposure to U.S. armored vehicle modernization — optics, periscopes, and sighting systems for Abrams, Bradley, XM157, and more

Works through primes like BAE Systems, General Dynamics, Vortex Optics

Margins expanding as pre-2020 IDIQs roll off

Profitable, cash-generating, supply-constrained, not demand-constrained

U.S.-made. FAR-compliant. Tariffs irrelevant

My fair value? ~$10/share — about 75% upside from here.

I never thought I’d care about who makes tank periscopes!

But Optex Systems (NASDAQ:OPXS) keeps showing up. $2M here. $4M there.

Backlog? Up again — now over a record $46M.

The pattern’s real: primes win 9-figure contracts → a few months later, Optex lands $2–5M suborders.

December 2024: BAE wins $656M for Bradley Fighting Vehicles

March 2025: Optex lands $4.2M to supply periscopes and optical systems for the same program

Now layer in Trump’s proposed $1T defense budget proposal and his push to cut procurement red tape — and suddenly delivery windows compress.

This won’t moon off one earnings report.

But it might quietly double while the rest of the market argues about Nvidia’s valuation.

Here’s what they actually do:

Optex runs two businesses.

Optex Systems (~50% of revenue) makes the hardware — periscopes, sighting systems, and night vision optics — that go into U.S. tanks and armored vehicles. These are the “eyes” of the vehicle.

Applied Optics Center (AOC) (~50% of revenue) handles the coatings — thin films that block harmful laser wavelengths and protect sensors and soldiers from optical damage. They also make laser filters for advanced scopes like the XM157.

Together, they cover both ends of the optical stack: what you see through, and what protects what you see with.

Follow the Primes

In their 10-K, Optex notes they supply periscopes, collimator assemblies, vision blocks, and laser interface filters for “almost all ground system platforms.” I took that literally.

I pulled the full list of U.S. ground systems from the FY2025 DoD budget and mapped each to its respective prime. The 2 tables below reflects those allocations — and yes, Optex touches nearly all of them.

Link—> Defense 2025 Budget

In just the first half of 2025, Optex announced two new contracts tied directly to major U.S. modernization programs. And the pattern is clear:

A prime wins a 9-figure contract → Optex follows with a multi-million-dollar subcontract.

🔭 $5.7M for Laser Filter Units — XM157 Program

PR Date: April 9, 2025

Program: NGSW-FC (Next Gen Squad Weapon – Fire Control)

Prime: Vortex Optics (Sheltered Wings Inc.)

Optex Division: Applied Optics Center (AOC)

Use Case: Laser protection filters for XM157 scopes

Prime Contract: $2.7B, 10-year IDIQ awarded in Jan 2022 (up to 250,000 units)

Runway: Through 2032 — real backlog longevity

This confirms Optex is now embedded not just in vehicles — but also in next-gen soldier systems.

🪖 $4.2M for Periscopes & Optical Sighting — Bradley A4

PR Date: March 19, 2025

Program: M2A4 / M7A4 Bradley Production

Prime: BAE Systems Land & Armaments L.P.

Prime Contract: $656M awarded in Dec 2024; runs through Nov 30, 2027

Optex Delivery Window: 28 months — aligns exactly with prime contract timeline

This confirms Optex's role as a recurring optics supplier into one of the U.S. Army’s core armored vehicle fleets.

These two awards alone total nearly $10M — but more importantly, they are live examples of backlog being refilled through real, funded DoD programs.

Don’t Forget Abrams Tank

Optex doesn’t break out revenue by platform, but Abrams has long been a core customer.

Prime: General Dynamics Land Systems (GDLS)

Prime Contract: $4.6B awarded in Dec 2020 for M1A2 SEPv3 production through June 2028

The 10-K flags a decline in Abrams funding as a risk. That’s incomplete.

FY2025 procurement is lower, but only because the Army is transitioning to the M1E3 variant. Meanwhile, GDLS continues to receive technical support and Foreign Military Sales (FMS) orders — which don’t show up in the core budget line.

Abrams isn't going away. It’s evolving. And Optex, historically embedded in its optical stack, is likely to stay with it.

🔎 Why This Research Matters

So what’s the point of tracking all this?

Because prime contract awards are the clearest forward signals for subcontractors like Optex.

Here’s a real example:

March 2025: BAE wins $188M to build 30 Amphibious Combat Vehicles (ACV) with turreted cannon variants

These are optics-heavy vehicles — ideal fit for Optex's product set

If history holds, a $2–5M follow-on order could hit Optex’s backlog by late 2025 or early 2026

🧭 How I Tracked All of This

To build conviction in Optex, I went beyond the filings.

I used defense.gov/contracts to track prime awards and match them to Optex’s timelines. I cross-referenced that with the FY2025 weapons budget and Optex’s own 10-K.

The insight? Prime contract flow is the best forward indicator of Optex’s backlog. Once you start connecting the dots, the pattern becomes hard to ignore.

🛡️ Why Optex’s Business Is Defensible

Optex doesn’t compete on flash — it competes on trust, qualification, and entrenched positioning.

Here’s what protects it:

Sole-source status on most U.S. periscope systems

ITAR-registered, CMMC-compliant, and holds a government-approved accounting system

Runs a cleared facility with the infrastructure to handle sensitive DoD optics work

Certified supplier to primes like BAE, General Dynamics, and Vortex Optics

In niche segments (periscopes, vision blocks) where volumes are high but ASPs are low — making backward integration unattractive for primes

At a recent LD Micro event, the CEO said it plainly:

"If you're a small company, there's too many barriers. If you're a large company, you're not going to backwards-integrate into a $1,500-per-unit space."

This is how Optex quietly defends its turf.

With bureaucracy. With qualification. With time.

And that’s exactly what makes it durable.

💰 Valuation & Setup

If you’ve followed my last two articles on ROIC and reinvestment, you know I’ve started viewing businesses through a quality lens — not just on valuation, but on how efficiently they deploy capital and how sustainably they can grow.

So I did the math for Optex.

I calculated NOPAT and Invested Capital to get to ROIC. Then I looked at how much of that profit gets reinvested — and from there, projected sustainable growth.

Here’s what I found:

👉 ROIC is rising

👉 Reinvestment is aggressive — ~100%

👉 ROIIC (Return on Incremental Invested Capital) is north of 40%

The numbers speak the narrative.

With a $46M+ backlog and new awards still coming in, Optex doesn’t need to chase growth. It’s structurally set up to deliver it — likely in the mid to high teens.

That’s what makes it interesting.

⚙️ 2025E Forecast

In its Q1 2025 press release, Optex said:

“We expect that our strong backlog, as detailed in our 10-Q, should allow the company to deliver revenue in excess of $38 million for fiscal 2025.”

I’m assuming they hit $40M — a reasonable base case, especially given award cadence and how conservative their guidance tends to be.

In FY2024, they did $34M in revenue and $3.7M in NOPAT (~10.9% margin).

Assuming modest margin improvement (legacy contracts rolling off), I estimate:

2025E NOPAT ≈ $4.5M on $40M revenue

+18% revenue growth

+22% NOPAT growth

How I Value It

I use a two-stage ROIC-driven DCF — not just plug-and-play FCF.

I assume a 10-year explicit forecast period, which mirrors the typical lifecycle of large DoD modernization programs like Bradley A4, AMPV, and Abrams SEPv3 upgrades. These programs often run across multi-year contracts with steady funding and backlog visibility — making a decade-long window both reasonable and realistic.

Also:

Free Cash Flow = NOPAT × (1 − Reinvestment Rate) = FCF - Net Investment

Because reinvested capital is not available to shareholders — it fuels growth.

✅ Stage 1: The Reinvestment Years (2025–2034)

For the first 10 years, Optex is in full expansion mode.

Years 1–5: NOPAT grows 15% per year, fueled by reinvestment into programs like XM157, Bradley, and Abrams. ROIICs ~ 20%.

Years 6–10: Growth slows to 10%, and ROIIC moderates to 15% — still comfortably above Optex’s 10% cost of capital (WACC).

Throughout this phase, 100% of NOPAT is reinvested to capture long-term defense tailwinds.

There’s minimal FCF in this phase — but value compounds via high-return reinvestment.

📉 Present Value of Stage 1 = PV of Free Cash Flow (Years 1–10)

🚀 Stage 2: The Payout Phase (Year 11 and Beyond)

Starting Year 11, Optex shifts into a more mature, capital-light phase:

Growth slows to 3%, roughly in line with historical DoD budget growth.

ROIC equals WACC (10%), meaning no further economic profit is generated.

Only 30% of NOPAT is reinvested to maintain 3% growth

(g / ROIC = 3% / 10%).The remaining 70% of NOPAT is distributed as FCF.

📉 Present Value of Stage 2 = PV of Continuing Value (Year 11+)

(Refer to my last article for the full framework)

📦 Total Enterprise Value = $70M

With ~7 million shares outstanding, that implies a fair value of ~$10/share — ~75% upside from the current price.

🧠 Wrapping It Up

This isn’t a moonshot. It’s a structurally sound defense subcontractor with:

A growing $46M+ backlog tied to multi-year DoD programs

Embedded exposure to platforms like Bradley, Abrams, and XM157

Expanding NOPAT, rising ROIC, and reinvestment that compounds value

A business that doesn’t rely on the market cycle — it runs on government contracts

At ~8x 2025E NOPAT, the market’s pricing in little growth, little durability, and no edge.

But the pattern is real: when the primes win, Optex follows.

And with defense budgets ramping, that pattern is just getting started.

The math checks out.

My Skin in the Game

Disclaimer

This is not financial advice. I hold positions in the stocks mentioned, which may create a conflict of interest. Please do your own research and consult a financial professional, as all investments carry risk, including potential loss of principal. I have not received any compensation from any company to write this; all opinions are solely my own.

Follow me on Twitter: @The10xRadar

great idea aditya, what about all the talks of drones? will these big vehicles be as needed?