The Little Company Poised for a 150%+ Breakout: Evome’s Bold Turnaround

From Acquisition Overload to Strategic Focus: How Shedding Debt is Fueling a Remarkable Comeback

The Big Picture: Tapping Into a $45 Billion Recovery Science Market

The U.S. recovery science market, valued at $45 billion with a 4% CAGR, is expanding rapidly. Spanning physical therapy, orthopedic care, and chiropractic centers, the sector’s growth is fueled by an aging population and advancements in rehabilitation technology. This fragmented space presents ripe opportunities for acquisitions and strategic partnerships as companies look to consolidate and scale.

Within this dynamic landscape, Evome Medical Technologies (TSX-V: EVMT) is positioning itself to seize growth through high-margin products in orthopedic and neurological rehabilitation. With a focused strategy of acquisitions and product licensing, Evome aims to capitalize on these expanding opportunities.

But the road to success wasn’t always so clear.

The Empire-Building Years (2021-2022): Six Companies. One Catastrophe.

Salona Global Medical Devices Corp. (now Evome Medical Technologies) once had big dreams. The company aggressively pursued an acquisition strategy, aiming to dominate the healthcare space and build an empire—fast. However, this rapid expansion came at a cost; when you move that quickly, things can spiral out of control. And that’s precisely what happened.

In 2021, under the leadership of Les Cross, Salona launched an acquisition spree, snapping up six companies in just 12 months. Six companies in one year—what were they thinking?

South Dakota Partners (SDP) – May 2021: The first domino. SDP, a contract manufacturer, was supposed to give Salona control over its supply chain. Instead, it brought more complexity than they could handle.

DaMar Plastics – May 2021: Acquired just days after SDP, DaMar added custom plastic molding to the mix. But why? It stretched resources and had little alignment with the core business.

Biodex Medical Systems – Mid-2021: Known for its gold-standard rehabilitation devices, Biodex was a major win on paper. Its System 4 line had earned a stellar reputation in the rehabilitation industry. But the company wasn’t ready for what came next. Integrating a global business like Biodex into Salona’s rapidly expanding portfolio proved to be a monumental challenge. Yet, despite the chaos that would soon follow, Biodex would later emerge as the very asset that could save the day. It wasn’t clear yet, but the future of this story would revolve around Biodex.

Mio-Guard – Mid-2021: A complementary player in sports medicine and injury recovery. More products meant more complexity, adding to the mounting challenge.

Simbex – Mid-2021: High-tech neurorehabilitation and monitoring systems. Cutting-edge tech with huge potential, but its value was lost amid the turmoil.

Arrowhead – Late 2021: Another acquisition that didn’t fit. Soon sold off when the financial cracks started showing.

In just one year, Salona’s aggressive acquisition spree led to mounting debt and operational chaos, turning a promising opportunity into a cautionary tale.

Fixated on acquisitions, Salona neglected the crucial task of building an integrated business. What could have been a leader in the medical device industry was left teetering on the brink of collapse, buried in debt and disarray.

Enter Mike Seckler: The Turnaround Specialist

Just when all hope seemed lost, Mike Seckler stepped onto the scene. With a proven track record at Ferring Pharmaceuticals, he was adept at transforming struggling divisions into success stories. Appointed Interim CEO in June 2023, Seckler faced an uphill battle: over $20 million in acquisition-related debt for a company valued at only $20 million—a recipe for disaster! For five consecutive quarters, revenue growth had stalled, and the business was mired in losses. In the middle of that chaos, he focused on the one thing that could turn everything around: Biodex—a powerful asset with the potential to drive the company’s revival.

Biodex: The Heart of the Turnaround

Biodex Medical Systems wasn't just another acquisition; it was the lifeblood of Evome’s portfolio. Renowned for its industry-leading rehabilitation devices, Biodex has garnered the trust of healthcare providers worldwide, establishing a strong reputation in physical therapy and neurorehabilitation markets. With over 15,000 customers and 52 distributors spanning 70+ countries, Biodex was perfectly positioned for expansion. Seckler quickly recognized that with Biodex, he had a solid foundation to rebuild Evome's credibility and market presence. His next challenge was aligning the rest of the business with this vision.

The Turnaround Begins: Execution and Early Wins

Armed with a clear plan, Seckler's strategy was straightforward: focus on Biodex, eliminate non-core assets, and streamline operations. By mid-2023, he began selling off non-core assets like Arrowhead and Simbex, which no longer aligned with the company’s objectives. Additionally, Seckler slashed operational expenses by over $2 million annually and secured better terms with key lenders, providing the company with crucial recovery time.

By late 2023, Seckler's emphasis on Biodex began to bear fruit. Revenue from this segment doubled, showcasing the effectiveness of centering the business around its strongest asset. To further stabilize the company, Seckler renegotiated debt terms, reducing interest payments and extending deadlines, which gave Evome the necessary breathing room for recovery.

As 2024 kicked off, Evome emerged as a leaner, more focused organization. While debt remained a challenge, I see that the distractions were cleared, positioning Biodex to spearhead growth efforts. In early to mid-2024, Seckler planned to divest two additional operating subsidiaries, South Dakota Partners Inc. and Mio-Guard LLC, further mitigating debt. This move was part of a larger strategy to eliminate non-core distractions and ensure that all resources were directed toward Evome’s most promising growth opportunities.

The Results Speak: Q2 2024

Fast forward to Q2 2024, and the impact of Seckler’s turnaround strategy was undeniable. Evome experienced a revenue surge, totaling $10.5 million, with $6.1 million generated from the core Biodex Rehab business—an impressive 59% increase from the previous quarter. Gross profit from Biodex also doubled, reaching $2.3 million. Crucially, Evome achieved positive adjusted EBITDA of $421,000, marking a significant turnaround from a $1.7 million loss in the prior quarter.

This success underscored the effectiveness of Seckler's cost-cutting measures and strategic focus. However, Evome still grapples with a daunting $14.8 million in acquisition-related debt, a combination of earn-out obligations and promissory notes tied to its past acquisitions. Despite achieving positive EBITDA, the company's current ratio of 0.55 and negative working capital reflect ongoing liquidity pressures, as cash reserves of CAD 1.07 million remain tight against the backdrop of its current liabilities.

This pressing financial burden ultimately sparked a call for one last decisive action—one that I believe will define Evome’s future.

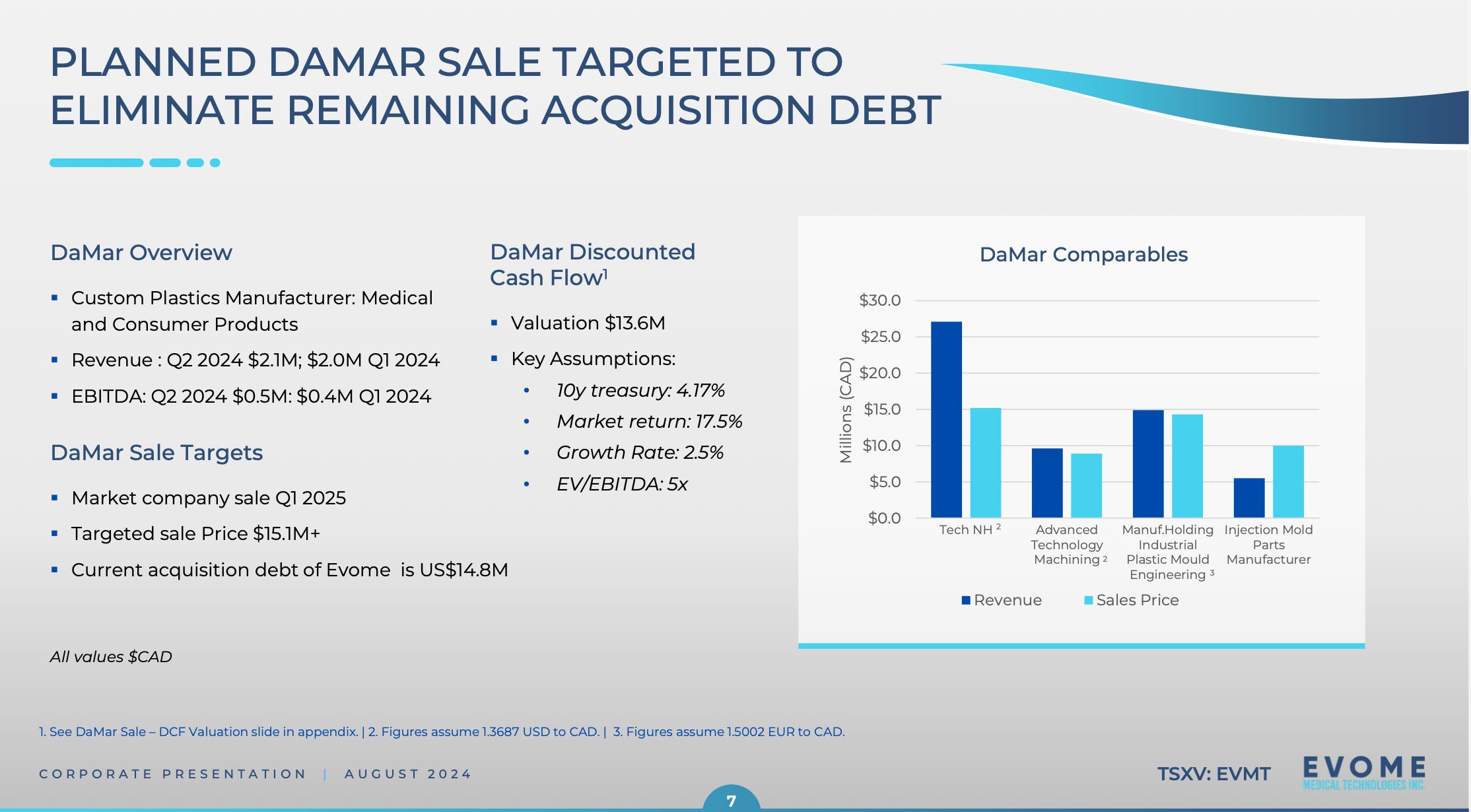

DaMar Sale: The Final Piece

Evome is poised to eliminate all of its acquisition-related debt by targeting the sale of DaMar Plastics by Q1 2025, aiming for $15.1 million or more. This sale is pivotal, as it will allow the company to shift its focus entirely to growth through the Biodex brand. Management is optimistic, and I share this sentiment; DaMar’s unique position as one of only two contract manufacturers in Southern California ensures strong demand and numerous potential buyers.

With CEO Mike Seckler already leading a transformative turnaround, the successful completion of this sale could be the defining moment for Evome. I believe the entire story hinges on this decisive action. If the sale goes through, Evome would be well-positioned to solidify its future, unlocking significant growth potential in the rehabilitation market.

Q3 2024: Signs of Stabilization and Debt Reduction

Looking ahead to projected Q3 2024, I believe Evome Medical Technologies continues to showcase clear signs of stabilization in its business operations, accompanied by a strategic focus on reducing debt. Management has presented projections indicating a positive trajectory, and I’m confident these figures emphasize the effectiveness of recent initiatives aimed at strengthening the company's financial foundation.

For more insights into the company’s vision and future direction, check out their latest presentation here on YouTube

A Clear Path Forward: Biodex as Evome's Growth Engine

With debt elimination on the horizon, Evome is poised to achieve annual revenues of $27.5 million, a gross profit of $10.9 million, and an adjusted EBITDA of $2.1 million in 2025. However, Seckler is not stopping there; he plans for ambitious growth. By leveraging Biodex’s strong reputation and extensive customer base, Seckler aims to penetrate new markets and introduce high-margin products.

With the Reactive Step Trainer already launched, Biodex is expanding its reach into the broader private physical therapy market, which holds a much larger customer base than its traditional institutional focus. Alongside this, the upcoming SpaceTek Knee, expected to be available by Q4 2024, is set to further strengthen their market position. Together, these innovative products target a total addressable market of approximately $3.0 billion, positioning Biodex to capitalize on substantial growth opportunities.

By licensing or acquiring one new product each quarter, Evome will enhance its offerings in orthopedic, neurological, and cardiopulmonary rehabilitation. This innovative white-labeling strategy will allow Biodex to attach its trusted name to new products with minimal capital investment, targeting gross margins of 25-40%. With 27 product targets identified, 16 discussions initiated, and 6 NDAs signed, Evome is laying the groundwork for revenue growth by 2025. For the first time in years, I believe the company will have the flexibility to reinvest in its core business and capitalize on opportunities in the global rehabilitation market.

Proven Strategy: Expanding Through Frequent Licensing and Acquisitions

Evome Medical Technologies is strategically positioned to thrive in the competitive recovery science market by employing a focused strategy of frequent licensing and acquisitions.

Larger companies like Medtronic and Stryker have employed similar strategies, completing multiple acquisitions to rapidly dominate their markets. While Evome operates on a smaller scale, its focus on acquiring high-margin products and leveraging Biodex’s extensive distribution network provides a clear path to accelerated growth. I also see Evome’s approach mirroring the success of companies like Align Technology, which started small and grew into global leaders by strategically acquiring complementary technologies.

To fund this expansion, I believe Evome is likely to use equity offerings, a common approach for companies seeking rapid scaling without over-leveraging through debt. This strategic move will enable Evome to seize acquisition opportunities while maintaining financial flexibility, positioning the company for long-term success.

Key Competitive Advantages for Evome

Evome’s competitive edge lies in its ability to focus on underserved segments of the rehabilitation market, particularly smaller physical therapy clinics and chiropractic centers, which represent 40% of the U.S. market. I believe this focus allows Evome to build deeper relationships and customer loyalty, setting it apart from larger competitors like Stryker and Medtronic, who primarily target hospitals and institutions.

By leveraging Biodex’s strong global reputation and extensive distribution network, I see Evome positioned to expand its market presence while introducing innovative products. The company’s agile strategy of licensing and acquiring new products quarterly ensures it stays ahead of market demands, positioning Evome as a nimble competitor in the evolving rehabilitation landscape.

Now, Let’s Dive into Valuation!

In evaluating Evome Medical Technologies, I’ve adopted a base case scenario based on the Biodex business proforma provided by the company. This scenario assumes no further growth beyond the projected 2025 baseline, which forecasts annual revenues of $27.5 million and an adjusted EBITDA of $2.1 million. Based on today's closing price of C$0.12, and assuming the complete elimination of all acquisition debt, I estimate Evome’s enterprise value (EV) at approximately $15 million.

This conservative approach is employed to highlight the substantial upside potential inherent in focusing solely on Biodex's current financial projections after the acquisition debt has been fully repaid, without factoring in any future growth or expansion opportunities. To establish a clearer valuation framework, I utilize a two-pronged approach with both EV/Sales and EV/EBITDA multiples. This comprehensive perspective helps assess the company's true value and growth potential while considering industry benchmarks and market dynamics.

EV/Sales

In the medical technology sector, the EV/Sales multiple averages between 4x and 5x. For instance, Stryker trades at roughly 6.7x, Medtronic at 4x, and Boston Scientific around 8.8x. These large, established players command premium valuations due to market dominance and strong cash flows.

For smaller companies like Evome, multiples can be lower. Recent acquisitions such as Natech Plastics, sold at 1.8x EV/Sales, indicate a valuation floor. Applying a conservative 1.5x EV/Sales multiple to Evome's current revenue projection implies a 150%+ potential upside from its current valuation. I believe this conservative estimate still presents substantial room for appreciation.

EV/EBITDA

Large-cap companies like Stryker (27x), Medtronic (16x), and Boston Scientific (36x) often trade at higher EV/EBITDA multiples, reflecting their consistent earnings. Smaller companies can still command significant multiples, as seen in recent deals like NuVasiv Inc.'s acquisition at 17.2x EV/EBITDA.

Using a cautious 15x EV/EBITDA multiple, I estimate Evome’s valuation to reflect a 100%+ upside from its current position. This reinforces my belief in the potential for substantial appreciation, even under conservative baseline assumptions.

Potential Risks

By now, the risks associated with Evome Medical Technologies should be evident. The company is grappling with a significant debt burden of approximately $14.8 million, which I believe poses a critical challenge. Although the planned divestiture of DaMar Plastics aims to alleviate this issue, I recognize that execution risks are inherent in any significant corporate transition.

Moreover, Evome's growth strategy hinges on the successful integration of new products and partnerships. The competitive landscape of the rehabilitation technology market raises uncertainty; there’s no guarantee that anticipated revenue from these initiatives will materialize as planned. This is something I’m closely monitoring.

If you're concerned about a potential capital raise, management has clearly stated they do not intend to raise funds to eliminate debt, as they believe the current stock price is undervalued. Instead, their strategy focuses on securing capital for growth only after the stock price reflects the company’s true value. Personally, I see this as a positive sign, as it indicates a commitment to building long-term value rather than merely addressing debt in the short term.

Conclusion: A Compelling Investment Opportunity

In summary, Evome Medical Technologies represents an intriguing investment opportunity. The projected upside of 150%+ is particularly compelling, especially given that these figures are based on conservative valuation assumptions.

Now, consider the potential if Mike Seckler and his team make tangible progress with Biodex—this could turn into a remarkable multibagger. Having closely followed this company for the past six months, I’ve witnessed firsthand how Seckler walks the talk. His strategic vision for leveraging the Biodex brand, combined with his disciplined approach to driving growth, fills me with optimism for the future. I firmly believe in the strength of this management team, which is why I’m personally invested. While there are risks to navigate, the potential for substantial value creation is increasingly apparent. The path forward looks promising, and I believe Evome is on the brink of something great.

My Skin in the Game: As you can see below, Evome makes up a significant portion of my portfolio, demonstrating the level of conviction I have in this company. I’m not just writing about Evome—I’m invested in its potential. If you’re looking for opportunities with real growth prospects, Evome is one I’m betting on for the long term.

If this deep dive into Evome sparked your interest, hit that like button, subscribe for more insights, and feel free to drop a comment with your thoughts or questions! I’d love to hear what you think about Evome and how you see the company evolving. Let’s keep the conversation going!

Disclaimer:

This is not financial advice. I hold positions in the stocks mentioned. Please conduct your own research, as all investments carry risk. I have not been paid by any company to write this; all opinions are my own.

"The Company’s intention is to submit an application for approval of the SpaceTek Knee™ Device with the U.S. Food and Drug Administration (the “FDA”) in early 2024." Has the device been approved?