The ROIC × Reinvestment Framework (Part 1)

A Practical Guide to Capital Efficiency — and the Lens I’m Learning to Use

Estimated Reading Time: 15 minutes

The Formula That Changed How I Invest:

ROIC × Reinvestment = Growth

There’s a moment every investor hits—usually after they’ve built a few DCFs, compared enough EV/EBITDA multiples, and watched a few “cheap” stocks stay cheap—where the question shifts.

You stop asking, “Is this stock undervalued?”

And start asking, “Is this even a good business?”

I hit that moment recently. As markets turned shaky, I revisited every position in my portfolio—not just to raise cash, but to make sure I owned the kinds of businesses I’d be excited to buy more of if prices dropped further.

That’s where this writeup begins.

Here in Part 1, I’ll break down the formula that reshaped how I think about business quality.

In a follow-up piece, I’ll take it a step further—and ask:

What kind of growth is the market already pricing in?

For a while, I leaned on the usual metrics: EV/EBITDA, EV/Sales, adjusted earnings. Like many newer investors, I told myself a compelling narrative could fill in the gaps. And to some degree, it worked—at least on the surface.

Guilty as charged. But I’m learning—and this past year has completely reshaped how I think about business quality and capital efficiency.

Because the companies that truly compound wealth don’t just look cheap.

They consistently turn capital into value—quietly, efficiently, and over time.

And just as importantly, they have somewhere productive to put that capital.

That’s what led me to a deceptively simple equation:

Sustainable Growth = ROIC × Reinvestment Ratio

A lot of my thinking was influenced by an excellent (and dense) Morgan Stanley report—Return on Invested Capital: How to Calculate ROIC and Handle Common Issues.

If you're curious, here's the link.

It might sound like a finance textbook formula, but it completely rewired how I think about capital allocation and long-term value creation.

Still, this framework only clicked when I applied it to real companies I thought I understood. If “cheap” stocks staying cheap has ever frustrated you, this lens might help.

🧭 What This Post Covers

In this piece, I’ll walk through:

Why adjusted metrics like EBITDA can mislead

What ROIC really measures—and how to calculate it

The reinvestment ratio, and how it completes the picture

Why ROIC × Reinvestment = Sustainable Growth

How this framework applies in real life:

Bird Construction (capital-intensive, cash-generating)

Talkspace (capital-light, potential high-ROIC SaaS)

Bird and Talkspace couldn’t be more different.

But both illustrate why ROIC—and the reinvestment opportunities behind it—tell a much deeper story than EBITDA ever could!

📉 Why Adjusted EBITDA Might Be Lying to You

How many earnings reports have you read that trumpet “adjusted” results?

Adjusted EBITDA (ignoring real costs)

Adjusted net income (pretending expenses don’t exist)

These metrics aren’t always wrong—but they often distract from a harder truth:

Revenue growth isn’t always profitable growth.

Company A grows slowly, funds it internally, and compounds.

Company B grows fast, boasts “record adjusted EBITDA,” and keeps raising capital.

Sound familiar?

That’s where ROIC cuts through the noise. It shows who’s compounding your capital—and who’s quietly consuming it.

Charlie Munger wasn’t wrong when he called EBITDA “bullshit earnings.” Not because it’s fake, but because it ignores the cost of growth—and that’s often the most important piece.

📐 Part 1: ROIC – The Quality of Return

Return on Invested Capital (ROIC) measures how efficiently a company turns every dollar of investment into after-tax operating profit (NOPAT). It’s one of the clearest lenses for understanding business quality.

Put differently:

ROIC tells you how many dollars of value a company generates for every dollar it puts to work.

And unlike EBITDA or EPS, ROIC strips away financial engineering. It ignores how a company is financed (debt vs equity), and focuses purely on the operating engine of the business.

A key benchmark here is the company’s Weighted Average Cost of Capital (WACC). Think of WACC as the minimum return that investors and lenders expect in exchange for providing capital. It’s like the company’s “hurdle rate.”

If a company’s ROIC exceeds its WACC, it’s creating value with every dollar it reinvests. But if ROIC falls below WACC, it’s quietly destroying value—even if earnings are growing.

The bigger and more durable the gap between ROIC and WACC, the more valuable the business becomes over time.

That’s why great businesses don’t just earn high returns—they consistently earn returns well above their cost of capital, and they find ways to reinvest at those rates for years. That spread is the engine behind real wealth creation.

🍋 The Lemonade Stand Test

You spend $100 on a stand, supplies, and ingredients. After one summer, you make $20 in real, after-tax profit.

ROIC = 20 / 100 = 20%

Your friend starts their own stand, spends $500, and earns $25.

ROIC = 25 / 500 = 5%

Your stand is the better business. Even though they made more revenue, you’re getting more return on each dollar invested.

That’s what ROIC reveals: not just growth, but how smartly capital is being used to create actual value.

The Anatomy of ROIC — How to Measure What Really Matters

At a high level:

But let’s break that down.

🔹 NOPAT: Net Operating Profit After Tax

NOPAT = EBITA - Cash Taxes (or) EBITA x (1 - Cash Tax Rate)

NOPAT represents the profits a company generates from its operations, assuming it has no debt and no excess cash. That means you're stripping out the effects of financial engineering—interest payments, leverage, and idle cash balances—and just focusing on what the business earns on its own merits.

NOPAT is the after-tax profit a company generates from its core operations, independent of capital structure.

To calculate it, you start with:

Operating Income (EBIT): Profit from core operations, before interest and taxes.

Add back: Amortization of acquired intangibles: These are legacy accounting charges—costs related to assets acquired from other companies (like old customer lists). The cost of maintaining these acquired assets is already captured in operating expenses.

Note: Do not add back amortization on internally developed assets (like capitalized R&D or internal-use software), as these reflect current investments and actual costs to support ongoing operations.

Add back: Embedded interest in lease expense — Under GAAP, lease interest is included in operating expenses, so we add it back to EBIT since it's a financing cost, not an operating one. Under IFRS, lease interest is already shown separately as a financing cost, below operating income, so no adjustment is needed.

Subtract: Cash taxes: Not the tax line from the income statement—actual cash paid. The amount of cash taxes paid by a corporation is typically shown at the bottom of the statement of cash flows or in the corporation’s notes to the financial statements.

Companies use two sets of rules:

Financial reporting (for investors) uses straight-line depreciation

Tax reporting (for the government) uses accelerated depreciation

This means taxable income is often lower than accounting income, so cash taxes paid are less than what’s reported in the income statement. That’s why, for ROIC, we subtract cash taxes, not book taxes.

What you don’t adjust for:

Depreciation: Real assets wear out. Keep it in. Especially if the company relies on physical infrastructure, like a manufacturer or contractor — depreciation reflects real economic cost.

Stock-based compensation: Non-cash, yes, but it dilutes ownership. It’s a real cost. Keep this in as well.

🔹 Invested Capital: The Capital That Powers the Business

If NOPAT is the engine’s output, Invested Capital is the fuel the company has poured in to generate it.

There are two equivalent ways to calculate it. I prefer the Operating Approach:

1. Operating Approach

This focuses on the assets actively used to run the business:

Net working capital (excluding non-interest-bearing liabilities like deferred revenue)

Tangible assets (PP&E)

Capitalized R&D or internal-use software

Acquired intangibles and Goodwill: I include goodwill because it reflects capital actually deployed, even if the company doesn’t realize the full benefit right away. It makes ROIC more conservative, which I’m okay with. If you paid for it, you should count it.

A small operating cash buffer (2–5% of revenue): For mature companies, 2% of revenue is a typical baseline. For less predictable or faster-growing businesses, up to 5% may be more appropriate.

To assess whether an item is operating in nature, it's important to refer to the notes to the financial statements.

Exclude:

Excess cash

Non-operating assets

This method helps track efficiency over time—how productively capital is deployed.

2. Financing Approach

This focuses on how the business is funded:

Invested Capital = Debt + Deferred Taxes + Equity

It tells you where the capital came from, but not how it’s being used. That’s why I prefer the operating view. Although the financing approach is easier to calculate, it can be very misleading—which I’ll show in the example calculations later on.

Bottom line: The goal is to isolate the return generated by the core operating engine of the business, relative to the capital required to run it.

🔁 Part 2: The Reinvestment Ratio – How Much Gets Put Back In

This tells you how much of the company’s after-tax operating profits are being plowed back into the business, excluding external funding like debt or equity issuance.

Investment here includes:

Net capital expenditures (CapEx minus depreciation)

Increases in working capital

Growth-oriented acquisitions

If ROIC is about quality, the reinvestment ratio is about quantity—how much of that high-return engine is being scaled.

🚀 Part 3: Putting It Together – The Compounding Engine

When you multiply ROIC by the reinvestment ratio, you get a company’s sustainable growth rate.

Let’s look at two companies:

Company A: 30% ROIC, reinvests 20% of NOPAT

→ Sustainable growth = 6%Company B: 15% ROIC, reinvests 80% of NOPAT

→ Sustainable growth = 12%

So even though Company A earns higher returns, Company B grows faster—because it’s reinvesting more of those profits at decent returns.

🧭 The Compounding Matrix

Here's how I think about it:

You can make money in any quadrant, but the strategy must fit the business. For me, the sweet spot is a company that can reinvest at high ROICs for a long time.

🧠 Applying the Framework in Real Life

This lens—ROIC × Reinvestment—now shapes how I view every business I analyze.

Especially when a stock looks “cheap.”

Because sometimes, cheap is just another word for going nowhere.

In the next section, I’ll walk through how this plays out in two companies I own:

Bird Construction – a Canadian contractor with stable returns and disciplined reinvestment

Talkspace – a digital mental health platform with improving capital efficiency

Different sectors. Different growth stories.

But the same fundamental question applies:

How efficiently do they convert capital into value—and can they keep doing it?

Bird Construction: Compounding with Discipline

Bird is a boots-on-the-ground builder—literally. It’s one of Canada’s leading construction firms, building everything from data centers to public infrastructure. It operates in a lower-margin, project-based, capital-intensive industry—not exactly the typical profile of a compounder.

But that’s what makes Bird so interesting.

Despite the odds, it’s become a quiet compounding machine, driven by disciplined bidding, operating leverage, and smart capital allocation.

Let’s walk through the ROIC math for 2023 and 2024—and see how a business like this manages to compound with discipline.

✅ Step 1: Estimate NOPAT

We start with Income from operations from the income statement

FY 2024 - CAD 146.5M

FY2023 - CAD 101.2M

(Note: I’m including equity-method income from the income statement because it reflects Bird’s core operating returns from its JV. Accordingly, I’ll also add Bird’s share of JV capital to Invested Capital, ensuring consistency between the numerator and denominator for ROIC calculation)

Add back: Amortization of acquired intangibles

FY 2024 - CAD 17.8M

FY2023 - CAD 6.0M

These are non-cash legacy costs and should be added back

For Embedded interest in lease expense, since Bird reports under IFRS, so lease interest is already treated as a financing cost—we don’t need to adjust for it.

Subtract Cash Taxes Paid: (from Cash Flow Statement)

FY 2024 - CAD 23.5M

FY2023 - CAD 4.7M

So, in summary:

✅ Step 2: Estimate Invested Capital

We use the operating approach to invested capital, which focuses on the capital actually used to run the business—not how it’s financed.

Here’s what we include:

Net working capital

FY 2024: CAD 190.4M

FY 2023: CAD 101.2 M

Net working capital includes operating assets (such as receivables, contract assets, inventory, and prepaid expenses) minus non-interest-bearing current liabilities (such as accounts payable, contract liabilities, and provisions).

To assess whether an item is operating in nature, it's important to refer to the notes to the financial statements. For example, under current assets, the line item "Other assets" primarily consists of a Total Return Swap (TRS) derivative. Since this is not related to core operations, it is excluded from the NWC calculation.

We exclude:

Cash (not an operating asset)

Tax receivables/payables (timing items)

Dividends payable, lease liabilities, and other financing-related items

Investment in equity accounted entities

FY 2024: CAD 14.3M

FY 2023: CAD 10.5M

Included to match inclusion of JV income in NOPAT.

Property, Plant & Equipment (incl. ROU assets)

FY 2024: CAD 190.1M

FY 2023: CAD 130.4M

Intangible Assets and Goodwill

FY 2024: CAD 237.6 M

FY 2023: CAD 102.4 M

We include these to reflect the full capital deployed—even if accounting goodwill doesn’t always correlate with value.

Operating cash buffer (~2% of revenue)

FY 2024: ~CAD 68 M

FY 2023: ~CAD 56 M

Represents estimated working liquidity; avoids overstating ROIC.

So, in summary:

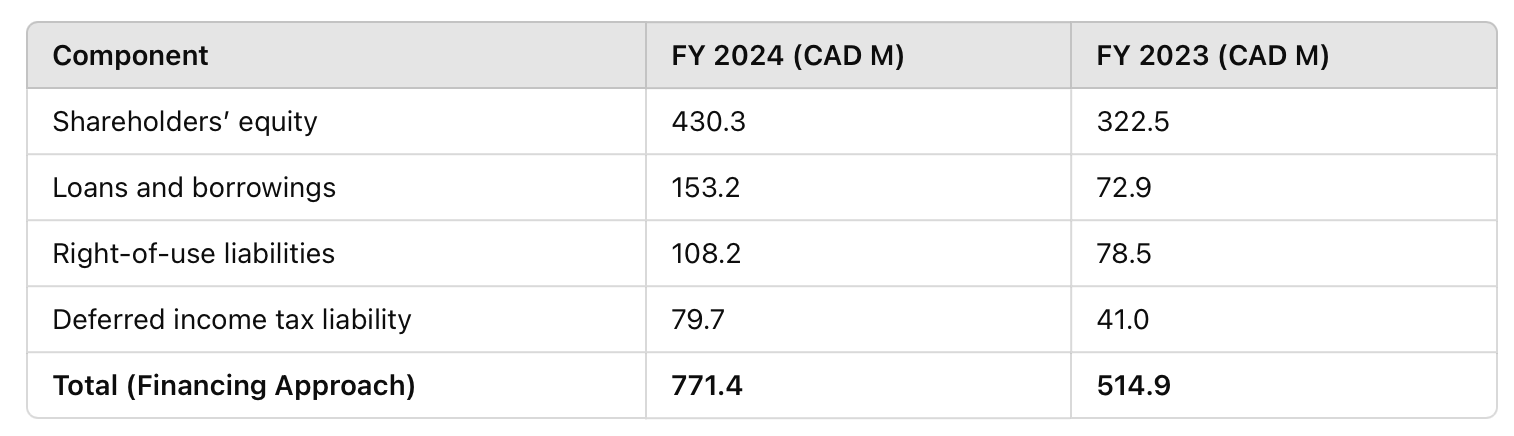

⚠️ A Note on the Financing Approach

Some investors calculate invested capital using the financing approach — simply adding up debt and equity. It’s quick, but it can be misleading for ROIC analysis.

Let’s see what that would look like for Bird:

Compare that to our operating approach, which yielded CAD 700M for FY 2024 and CAD 400M for FY 2023.

That’s a difference of +$71M in 2024 and +$114M in 2023 — primarily driven by two factors:

Inclusion of financing obligations such as lease liabilities and deferred taxes.

Lack of explicit isolation of productive operating capital like working capital and JV investments, which are essential for generating operating profit.

The financing approach just adds up everything—debt, equity, leases, deferred taxes—without showing which parts are really working in operations. In contrast, the operating approach explicitly isolates operating assets like working capital and JV investments that generate profit. That’s why I prefer the operating approach for measuring ROIC.

✅ Return on Invested Capital (ROIC)

ROIC = NOPAT / Invested Capital

I ran the numbers for 2021 through 2024:

In 2024, Bird made a sizable acquisition that contributed to the CAD 300M rise in invested capital. While not the sole driver, it was a key factor. As earnings normalize, ROIC should trend back toward the 25% range. A 20–25% ROIC band looks like a realistic long-term level.

📈 Incremental ROIC (ROIIC)

To gauge the quality of new capital deployment, I calculated the Return on Incremental Invested Capital (ROIIC), defined as the change in NOPAT divided by the increase in invested capital from the prior period.

Period 2023 —> 2024 ROIIC = (141 – 103) / (400 – 297) = 37%

Period 2022 —> 2023 ROIIC = (103 - 66) / (297 - 245) = 71%

2023 was a standout year, delivering exceptionally high returns on new capital. Although ROIIC tapered in 2024, it remained well above Bird’s cost of capital—easily 3 to 4 times its WACC—demonstrating that new investments are still strongly value-creating, even with acquisition dilution.

✅ Sustainable Growth Rate

Sustainable Growth = ROIC × Reinvestment Ratio

Let’s estimate the reinvestment ratio:

Reinvestment Ratio for 2024 = 300 / 141 = ~2.1 or 210%

Reinvestment Ratio for 2023 = 103 / 104 = ~1 or 100%

Reinvestment Ratio for 2022 = 66 / 51 = ~1.3 or 130%

So yes, Bird reinvested more than 2x its operating profit in 2024, primarily due to acquisitions funded by modest leverage and retained earnings.

Looking at the full 3-year period, the biggest drivers of capital growth were:

Net Working Capital (project mobilization, backlog)

Goodwill (acquisition-related)

Management targets a ~33% dividend payout, so we can reasonably assume the remaining ~67% of earnings are reinvested.

Let’s call it 70% for simplicity.

Sustainable Growth = 20% ROIC × 70% Reinvestment = ~14%

In its 2027 outlook, Bird guided to:

10% ± 2% annual revenue growth

→ Midpoint = 10%

That’s impressively consistent with the 14% implied sustainable growth from our capital efficiency model.

And the ~4-point gap makes sense.

Why? Because Bird’s backlog carries higher embedded margins, which means:

NOPAT is compounding faster than revenue

Operating leverage is kicking in

Higher-margin projects are ramping through the P&L

🔍 Bottom Line

Bird isn’t just managing projects—it’s compounding capital with discipline. That’s what makes it such a compelling business. With:

Core ROIC: 20–25%

Incremental ROIC: 30%+

Steady-State Reinvestment: ~70%

Implied Growth: ~14%

Additionally, management has repeatedly emphasized that they’ve conducted a forensic analysis of potential tariff impacts and negotiated robust cost pass-through terms. This means Bird’s margins are relatively shielded from tariff shocks, further enhancing its investment appeal.

But is the market recognizing that?

That’s the question I’ll explore in a follow-up writeup—where I’ll use this same framework to unpack what kind of growth the market is actually pricing in.

Talkspace: The Early Signals of Capital-Light Compounding

Talkspace is a virtual behavioral health platform that connects patients with licensed therapists and psychiatrists through text, video, and asynchronous messaging.

Unlike Bird, Talkspace doesn’t carry inventory or operate heavy equipment. Its capital base is lean by design. But that’s exactly what makes it compelling: if the model works, and operating leverage plays out, this could be a high-ROIC, capital-light compounding machine.

Let’s run the numbers for 2023 and 2024—and then use 2025 guidance to estimate where ROIC, reinvestment, and growth could be headed.

✅ Step 1: Estimate NOPAT

We start with Income from operations from the income statement

FY 2024 - $(4.5M)

FY2023 - $(23M)

Add back: Amortization of acquired intangibles

FY 2024 - $0.4M

FY2023 - $0.7M

These are non-cash legacy costs and should be added back

For Embedded interest in lease expense: For Talkspace, operating lease costs are minimal, and the embedded interest is likely immaterial for the overall ROIC calculation.

Subtract Cash Taxes Paid: (from Cash Flow Statement)

FY 2024 - $0.1M

FY2023 - $0.2M

So, in summary:

✅ Step 2: Estimate Invested Capital

We use the operating approach to invested capital, which focuses on the capital actually used to run the business—not how it’s financed.

Here’s what we include:

Net working capital

FY 2024: $(6.7M)

FY 2023: $(5.7M)

This includes operating assets (like Accounts receivable, other current assets) minus non-interest-bearing current liabilities (accounts payable, accrued liabilities, deferred revenue)

Note: A negative NWC is typical for subscription or prepayment-based business models and supports strong ROIC (efficient cash use).

Other long term assets - Includes fixed assets, intangible assets and ROU assets)

FY 2024: $8.5M

FY 2023: $2.4M

Operating cash buffer (~5% of revenue)

FY 2024: ~$9M

FY 2023: ~$7.5M

Represents estimated working liquidity; avoids overstating ROIC. I apply a 5% operating cash buffer for Talkspace (vs. 2% for Bird) to reflect its earlier stage and greater need for working liquidity.

So, in summary:

✅ Return on Invested Capital (ROIC)

ROIC = NOPAT / Invested Capital

While the core capital base remains highly efficient, Talkspace is still operating at a loss. That means ROIC is currently negative, but the invested capital base is so lean that marginal profitability could flip ROIC positive quickly.

✅ Forward ROIC Based on 2025 Guidance

Company guidance:

Revenue: $220M to $235M (17-25% increase YoY)

Adjusted EBITDA: $14M to $20M

We’ll make a few reasonable assumptions:

Total D&A: ~$1M (average of the last two years as a proxy)

Amortization of intangibles: ~$0.3M (non-cash and added back)

Cash taxes: ~$0.2M (Talkspace has NOLs that minimize tax liability)

Stock-based compensation: ~$10M (vs. $8.4M in 2023 and $9.1M in 2024)

NOPAT = Adjusted EBITDA – SBC – Cash Taxes – D&A + Amortization of Intangibles

NOPAT Estimate:

Low end: $14M – $10M – $0.2M – $1M + $0.3M = $3.1M

High end: $20M – $10M – $0.2M – $1M + $0.3M = $9.1M

Taking the midpoint of this range, we anchor on ~$6M as a base case for 2025 NOPAT.

We assume 2025 invested capital increases roughly in line with revenue (~25%), bringing it to ~$13M, up from $10.8M in 2024. This reflects modest scaling in platform infrastructure, sales capacity, and working capital needs.

Forward ROIC (assuming 2025 invested capital = $13M) = 6 / 13 = ~45%

This is a strong forward ROIC, especially for a company that only recently turned the corner on profitability. It highlights Talkspace’s capital-light model and growing ability to generate meaningful returns on incremental investment.

✅ Sustainable Growth Rate

Sustainable Growth = ROIC × Reinvestment Ratio

Let’s estimate the reinvestment ratio:

We already anchored on a midpoint NOPAT of $6M and assume invested capital grows from $10.8M to $13M — a $2.2M increase.

Reinvestment Ratio = 2.2 / 6 = ~37%

Following the Morgan Stanley ROIC framework, Talkspace already capitalizes internal-use software as part of invested capital. However, I’ve not capitalized R&D or sales & marketing in this base case—even though both are essential drivers of future growth. Morgan Stanley notes that for SaaS and subscription-based businesses like Talkspace, sales and marketing often act like capex, acquiring customers who generate recurring, long-term revenue streams.

As a result, the reported reinvestment ratio (~37%) likely understates true reinvestment, which is probably closer to 50–60% when you factor in these expensed, growth-oriented investments.

ROIC may come down slightly as Talkspace invests more aggressively—since invested capital would increase if we were to capitalize R&D or S&M—but the base case calculation still offers a useful anchor:

Sustainable Growth = 45% ROIC × 37% Reinvestment = ~17%

That supports a reasonable forward growth range of 17–20%, depending on how aggressively the company reinvests and how returns scale with that investment, which is line with the company’s forward projections

🔍 Bottom Line

Talkspace isn’t just delivering therapy—it’s building a capital-efficient, high-return platform. With:

Core ROIC: ~40% + (projected)

Sustainable Growth: ~17–20%

Minimal capital needs and meaningful operating leverage

A long reinvestment runway ahead

With profitability just beginning to inflect, the real question becomes:

👉 If this is what Talkspace is becoming… is the market giving it any credit?

That’s what I’ll explore in a follow-up writeup—using the same ROIC × Reinvestment lens to decode what kind of growth is already priced in.

Summary

I know this was a long one—thanks for sticking with it.

But if there’s one core takeaway, it’s this:

Great businesses aren’t just built on growth. They’re built on how well that growth is funded.

ROIC × Reinvestment isn’t just a formula—it’s a framework for finding real compounders.

And that’s where this lens becomes even more powerful—not just as a measure of business quality, but as a tool for valuation.

Not just to understand a company, but to decode what’s already priced in.

I’ll explore that in a separate follow-up—where I use this same lens to reverse-engineer market expectations, and ask:

👉 What kind of growth are investors really betting on?

That’s how I invest now.

Follow along for Part 2—where we decode the price tags behind the businesses we just analyzed.

Disclaimer

This content is for informational purposes only and does not constitute financial advice. I hold positions in the stocks mentioned, which may present a conflict of interest.

Please do your own research and consult a licensed financial advisor before making any investment decisions. All investments carry risk, including the potential loss of capital.

I have not received any compensation from the companies mentioned. All opinions are my own.

I really don't know how this post doesn't have dozens of likes and lots of comments, excellent and very clear writing. Thank you!!