Willdan Group: Why This Overlooked Stock Has 50%+ Upside Potential

Grid Modernization, Decarbonization, and a Strong Balance Sheet Make This Stock a Standout Opportunity

Estimated Reading Time: 5 minutes

Happy New Year! 🎉 I hope 2025 is off to a fantastic start for you.

Just a month ago, I shared the exciting news that this Substack had surpassed 100 subscribers. Fast forward another month, and we’ve more than doubled that! I’m thrilled to announce that we’ve now reached 250 subscribers in just three months.

This Substack began as my personal diary—a space to document discoveries and share the rigorous research I’ve honed during my first year of investing. Knowing that so many of you have joined me on this journey is both humbling and inspiring.

Thank you for being here!

Now, let’s kick off the year with a company that perfectly embodies my love for discovery.

I tweeted this a while back, and I still stand by it. Today, I want to highlight a company that lives up to this principle: Willdan Group (NASDAQ: WLDN).

Here’s the scoop:

A boring business growing steadily with zero fanfare.

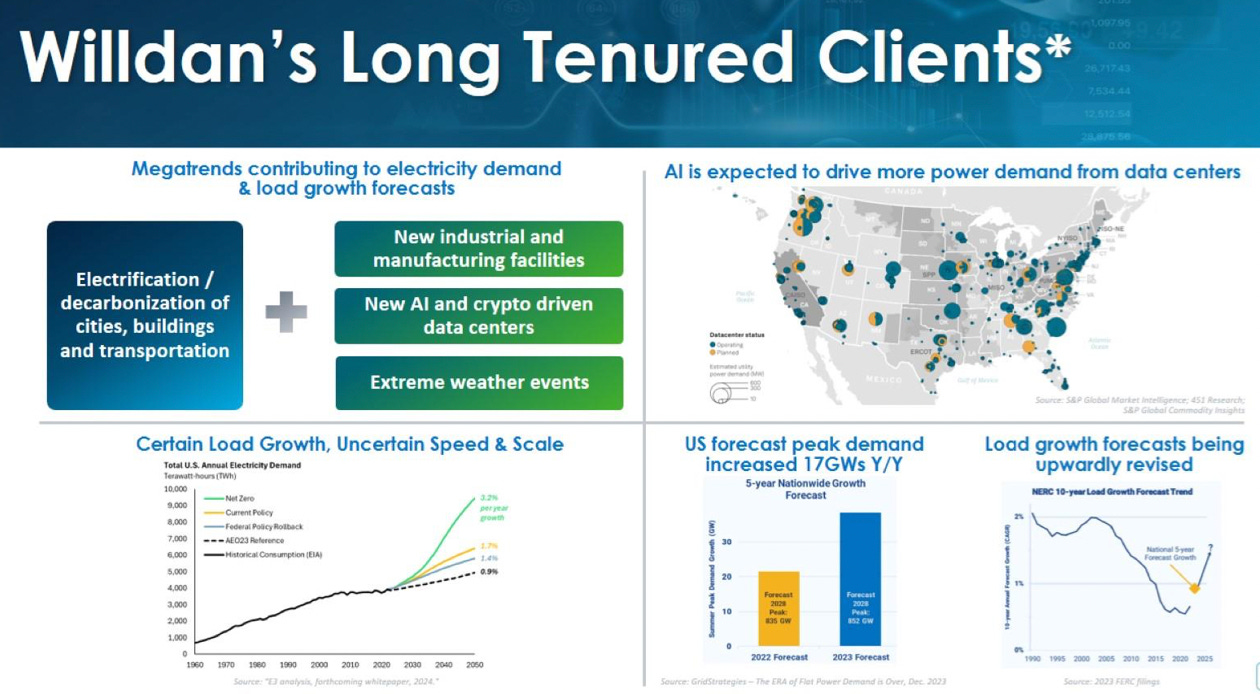

It’s helping cities decarbonize, upgrade power grids, and optimize energy systems.

It’s riding perfect market tailwinds, including electrification, decarbonization mandates, and skyrocketing energy demand from AI-driven data centers.

It’s trading at just ~10x 2025E EV/EBITDA.

And yet, no one seems to care.

Let’s fix that.

What Does Willdan Group Do?

Willdan is an engineering and consulting firm that works with governments, utilities, and businesses. They’re the ones tackling challenges like grid modernization, decarbonization, and energy efficiency.

In plain terms: Willdan helps the lights stay on, the power bills stay lower, and the planet get greener.

Here’s a snapshot of their business:

Revenue mix: 84% from energy services (efficiency and decarbonization), 16% from engineering projects.

Client mix: 50% state/local governments, 43% utilities, 7% commercial clients.

Key clients: Long-term partnerships with major names like NYPA, Consolidated Edison, and LADWP, proving their expertise in the nation’s largest markets like California and New York.

And then there’s their secret weapon: Integral Analytics, a proprietary software division with tools like LoadSEER that utilities use to optimize grids and integrate renewables.

This isn’t a flashy business. It’s just solid, growing, and essential.

In a fragmented marketplace, Willdan has carved out a unique niche by offering end-to-end solutions. Here’s what the competition looks like:

Policy and Data Analytics: Firms like Guidehouse and McKinsey dominate here.

Engineering: Players like CLEAResult and Resource Innovations compete in efficiency programs.

Program Management: Heavyweights like Burns & McDonnell and Siemens focus on managing energy projects.

But Willdan’s differentiation lies in integrating these services seamlessly. They’re not just a cog in the wheel—they’re the engine that drives projects from policy to execution.

Why Should You Care?

Here’s why Willdan is worth a closer look:

1. Electrification and Decarbonization

Cities are electrifying buses, buildings, and transit systems. Net-zero mandates are rolling out nationwide. Willdan is at the center of it all, with projects like helping New York implement Local Law 97, a massive decarbonization effort targeting public buildings.

As electricity prices skyrocket (PG&E (California) rates are up 87% since 2019), the demand for energy efficiency—Willdan’s bread and butter—is only increasing.

2. AI and Data Centers

AI isn’t just transforming the internet; it’s driving up energy demand. Data centers require massive power consumption, and companies like Meta are turning to Willdan for help optimizing energy use and reducing emissions.

The recent acquisition of Enica Engineering strengthens Willdan’s capabilities in this fast-growing commercial sector. Management has reiterated plans to pursue further acquisitions to grow its presence in the data center market and make commercial clients a larger portion of the revenue mix.

3. Stable Funding, Stable Growth

Willdan’s revenue is backed by long-term, stable funding mechanisms. Utility fees and government programs ensure consistent demand, and multi-year contracts provide visibility for years to come.

While it doesn’t receive IRA funding directly, Willdan helps clients secure it, driving consistent demand and long-term growth opportunities.

Financial Highlights

Willdan’s numbers speak for themselves:

2024 projected net revenue: $290M (+7.5% YoY).

2024 adjusted EBITDA: $53M (+16% YoY).

2024 adjusted EBITDA margins: 18%+ (up from 16% in 2023).

The company generates exceptional cash flow, with operating cash flow nearly matching adjusted EBITDA.

On the balance sheet, Willdan is rock solid:

Leverage ratio: 0.7x EBITDA.

Liquidity: $103M, including a $50M untapped credit line.

Here’s what’s refreshing: Willdan is cutting debt faster than most of us pay off credit cards. They started 2024 with $75M in net debt. By Q3, that number was down to $39M. Management used operating cash flow—not equity dilution—to pay it off. That’s rare for a small-cap company.

While Willdan’s year-to-date performance has been strong, it’s worth noting that Q4 2024 faces tough year-over-year comparisons due to an exceptional Q4 2023 performance, which management has flagged as a headwind. Despite this potential short-term dip, the company’s long-term growth trajectory remains intact, supported by stable contracts and favorable industry trends.

The Valuation Game

Here’s where things get interesting.

I see the company as a ~10% CAGR business over the long term (including acquisitions).

Let’s run the numbers:

2025E net revenue: $320M (+10% YoY).

2025E adjusted EBITDA: $60M (~19% margin).

Willdan currently trades at ~10x 2025E EV/EBITDA, compared to peers in the engineering and energy services sectors, which average 15x. Apply a 15x multiple—50% upside from today.

What makes this particularly interesting: this doesn’t even factor in potential upside from Integral Analytics or new projects funded by the Inflation Reduction Act (IRA).

An Often-Overlooked Area of Growth

Willdan isn’t just a services firm—it’s also a rising star in software. Heard of Integral Analytics?

Most of Wall Street hasn’t either.

This division develops high-margin grid analytics software that utilities rely on to forecast energy demand and plan for challenges like EV adoption and battery storage.

In Q3 2024, Integral Analytics generated $4 million in revenue—a modest number, but with exceptional gross margins and rapid growth. As the energy sector increasingly depends on data-driven solutions, Willdan holds one of the industry’s top tools.

The synergy is clear: every new project Willdan secures introduces utilities to LoadSEER, Integral Analytics’ flagship AI-driven platform for modeling energy demand and optimizing distributed energy resources.

As renewable energy integration and grid complexity grow, so does the necessity for tools like LoadSEER.

Here’s why this could significantly impact their growth trajectory:

Software revenue is not only high-margin but also scaling quickly.

The flywheel effect: more projects mean more utilities adopting Integral Analytics’ solutions.

AI-driven grid optimization is becoming indispensable, setting up exponential demand for LoadSEER.

This is the engine driving Willdan’s next phase of growth—and it’s just getting started.

Conclusion

So, why isn’t this a $50 stock?

It’s probably the usual story: it’s boring, small, and underfollowed. Big funds don’t want to bother with a ~$500M market cap. Retail investors want shiny tech stocks, not consulting firms.

But boring isn’t bad. Boring is often where the best opportunities hide.

If you’re willing to go to the overlooked corners of the market, there’s value to be found. Willdan Group is one of those corners.

My Skin in the Game

I own shares in Willdan because it’s a solid, undervalued business positioned at the intersection of energy transition and infrastructure modernization.

Disclaimer

This is not financial advice. I hold positions in the stocks mentioned, which may create a conflict of interest. Please do your own research and consult a financial professional, as all investments carry risk, including potential loss of principal. I have not received any compensation from any company to write this; all opinions are solely my own.

Follow me on Twitter: @The10xRadar

Nice write-up. Pinged you on Twix also. I am considering a write-up of this on my own newsletter after a friend shared your article with me. Any idea what the revenue growth may look like for Integral Analytics the next few years? They seem to have had success with the cross-sell.

Just subscribed to your newsletter!